The missing recession of 2023 remains unaccounted for. For some, it has already been and gone, while others await its full impact. Economic performance has varied significantly by geography, with US growth accelerating during the year fuelled by abundant energy and a fiscal boost. With bond yields falling in Q4 as the Fed gave explicit pivot signals, capital rushed to risk assets, a process that has paused so far in 2024.

Europe has also benefited from lower energy prices, but less directly and with a delayed impact. Without the fiscally driven stimulus of the US, its economies have been sluggish, with some dipping into recession. Notably, the UK outperformed the consensus view and continued to perform within the pack of the G7 economies. Europe’s economic outlook depends on two main questions: how soon rate cuts come and the true nature of China’s sluggish economy.

So far this year, the outlook for falling rates has been pushed back from the end of Q1 to Q2 or Q3. While this delay is a hindrance for most, it will be existential for others. As the perma-bears at Ruffer Investment Management have pointed out, governments are the only keen borrowers at 5.25%. Fed Chair Powell conceded at Jackson Hole that current interest rates are above the R* equilibrium level, which means the current policy risks things breaking.

So why did the Fed signal such a sharp about-turn on rates in October last year? They were either spooked by something we can’t see or think inflation has been slain. But why wait? Why not cut rates now? The answer is twofold. First, the Central Banks are determined to be Paul Volcker and not Arthur Burns; and second, why cut now when just saying you are going to cut does the job with falling bond yields? While this move proved an effective head fake for bond investors pre-Christmas, it is proving less effective over time.

Despite media focus on the increasing conflict and rising tensions in the Middle East, the direction of travel for inflation remains critically dependent on China. Oil and industrial commodity prices are weak, and although there are emerging supply chain issues, companies continue report the beneficial impact of moderating inflation, with Chinese and Eurozone producer prices well into deflationary territory. Despite China announcing several bazooka-like measures to stimulate its economy and boost its flagging stock markets, there are no current signs of success.

At its heart, China’s housing market, which has grown from nowhere twenty-five years ago to one of the world’s largest asset classes, faces multiple problems. A declining working-age population, a decreasing rate of household formation, over-building, excess debt and falling values mean that China’s consumers must rebuild their balance sheets. Having come out of lockdown without the excess savings cushion enjoyed by Western consumers, China’s extraordinarily high propensity to save negates its stimulus measures. Are China’s problems containable, or will they spill into the broader global economy? A deflationary impulse from China is welcome and inevitable. However, a re-run of the 1998 Asian Debt Crisis is not but is a tail risk.

Although it is proving sticky, UK inflation is heading down. Indeed, Capital Economics forecasts that it could be as low as 1.7% by April due to the energy price cap regime and 2023 base effects. With policy rates at 5.25%, wage growth at 6.5%, inflation below target and government borrowing below forecast, this is a positive set-up for an expansionary pre-election UK Budget in March.

Elections could significantly influence the outturn for economies and markets in several regions in 2024. As Trump marches through the Republican Primaries and the rising popularity of the AfD in Germany and the Nationalists in France suggest, both the EU and the US must deal with rising populism. The Democrat’s favourite Wall Street banker, Jamie Dimon, pointed out in Davos last week that Trump has been “kind of right” about some critical issues and suggested that whatever they thought of him, they should be more respectful of him. He signalled that populism’s appeal is reflexive, and the more they are threatened with obstructions to ballot papers, the more popular they become. As the UK learnt eight years ago, the populist appeal is less about political extremism and more about a protest vote against perceived patronising elites.

While one does not wish for political upheaval anywhere, the prospects for constitutional crises rise as democratic processes become stressed. In contrast, the UK will have its first General Election in memory when the divisive issue of its relationship with Europe will not be a primary campaign issue. Whatever we might think of the UK’s domestic political problems or the expected election outcome, the UK’s transition of power will score well against other democratic benchmarks. In the minds of global investors seeking certainty, this should be sufficient to boost net capital flows to the UK.

We know about the concentration of the US stock market, with seven enormous technology titans, AKA The Magnificent Seven accounting for such an enormous proportion of the market’s value. However, the Deutsche Numis Indices Annual Review 2023 shows that the UK market is, in fact, even more concentrated, exacerbated by a lack of new joiners and the persistent de-rating of domestic businesses relative to its remaining international majors. If yield curves revert to normal as policy rates reduce it is rational to expect equity returns to disperse and concentration to reduce.

The world has missed several years of the “smaller companies’ effect,” and the UK more than most. The AIM market has experienced its third straight year of decline. None of which means 2024 will see these trends reverse. However, increased global allocations to the UK, a reversal of outflows into fixed-income as rates moderate and a recovery of new issue opportunities could all help deliver a much-improved outlook for UK smaller companies and the long-awaited re-assertion of their long-run positive performance effect. We believe the much-improved performance in Q3 last year is a foretaste of what lies ahead.

Written by Jeremy McKeown

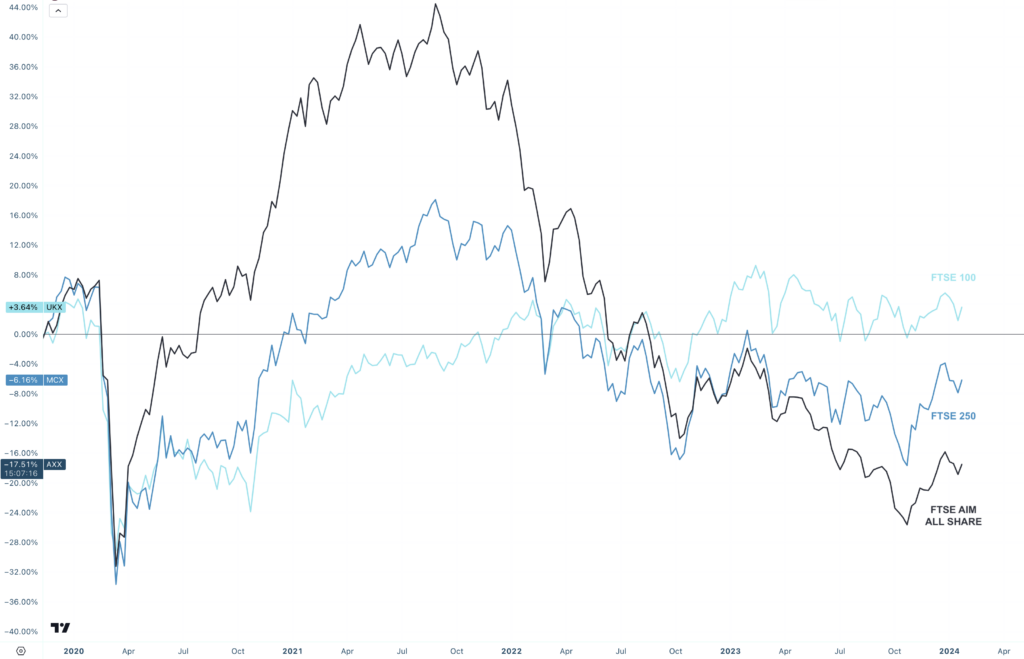

Jackson’s Chart: THE SMALL CAP FLIPPENING (An Analysis by Jackson Wray)

Explanation

In recent issues of the Curious Investor, we have identified trends and areas of importance across different markets. This week we are focusing on the “flippening” size preference in the UK equity market since 2020. Taking the three broad indices, the FTSE100 (light blue), FTSE250 (blue) and the FTSE Aim All Share (dark blue) and their movement since their congested Covid lows. Towards the end of 2020, as markets reacted to news of the first vaccines, the AIM All Share significantly outperformed its larger peers, opening a clear lead by the smaller end of the market to the large during most of 2021. However, concerns about rising rates and lower liquidity levels saw the closing of this gap into 2022, and dominance flipped to larger companies. A steady performance of the FTSE 100 continued, while the FTSE250 and, more so, the AIM All Share experienced sharp relative underperformance. From the October 2022 “Truss Crisis” lows, the larger FTSE 100 and 250 indices have shown more stability. However, the AIM market continued down and reached a new low by October 2023, the moment of the Fed rate pivot. As all markets recovered from this point, the relative performance flipped noticeably in favour of the smaller indices for the last two months of the year. 2024 has begun with a pause in rate expectations and equity market recovery. As we go through the year, the prospects for lower rates should once again reassert the relative strength of the smaller indices.

Further Reading & Listening:

DISCLAIMER

This is for information purposes only and is not to be considered as advice in any form, including but not limited to investment, accounting, tax, legal or regulatory advice. The information does not take into account a persons specific investment objectives, financial situation or particular needs of any specific recipient. Opinions expressed are our current opinions as of the date appearing on the document only.

Any working examples, forecasts or data are for illustrative purposes only. Dowgate Wealth does not make representation that the information provided is appropriate for use in all jurisdictions or by all Investors or other potential Investors. Parties are therefore responsible for compliance with applicable local laws and regulations. Dowgate Wealth will not be held liable for any loss or damage resulting directly or indirectly from the use of any information on this site.