One of the ways of reducing your taxable estate where you retain ownership of the investments and income derived from them is to have an inheritance tax portfolio. Dowgate Wealth offers a discretionary IHT portfolio service that is simple and cost effective.

Efficient digital infrastructure to maximise output and deliver best-execution for our clients

Optimized onboarding process to ensure a quick, seamless and stress-free experience

Direct contact to a dedicated member of the team who will be with you every step of the way. It is important to know that you are not just a number

Dedication to understanding that each client is unique and so are their objectives

Wealth of experience across different products and service types such as SIPP’s & ISA’s

Industry connections developed over years providing regular access to management teams and analysts

Relationships with academics provide enhanced investment due diligence

Reputation as long-term investors allow for unique opportunities such as being offered new equity issues

Proven track record regardless of market cycle

ISA’s are tax-efficient savings and investment accounts. You can use them to save cash or invest in stocks and shares. You can pay your whole allowance of £20,000 into a cash ISA or into a Stocks and Shares ISA or any combination of these as long as you do not exceed your annual allowance. The benefit and attractions of doing this are that you pay no Income Tax on the interest accrued or dividends received from an ISA and any profits from investments can be taken free of Capital Gains Tax. You must be 18 and older and resident in the UK in order to qualify.

You can now have a flexible ISA which lets you withdraw and replace money from your ISA, provided it is done within the same financial year. Not all ISA providers will let you do this but we have this facility available. Please be advised this is only available for Cash ISA and Stocks and Shares ISA.

Junior ISA’s are a great way of saving for your children in a tax-efficient way. Family and friends can contribute up to £9,000 into the account on behalf of the child in the 2023-2024 tax year. There’s no Income Tax or Capital Gains Tax to pay on the interest or investment gains.

Junior ISA’s are available to any child under 18 living in the UK who doesn’t qualify for a Child Trust Fund. Your child will qualify for a CTF if your child was born between 1 September 2002 and 2nd January 2011. Parents with a Child Trust Fund can now transfer to a JISA.

This is also known as a DIY pension. By having a SIPP you are able to invest in almost anything you like, making your own decisions and managing it yourself. Having a SIPP is more flexible than having a more traditional pension but there is also more risk and responsibility on you having to make your own investment choices. This is why most who want the flexibility then appoint an Investment Manager, such as ourselves, to undertake the investments and manage the portfolio on their behalf.

SIPP’s do not attract Capital Gains Tax and there is tax relief on your contributions depending on your rate of tax.

A Small Self Administered Scheme is essentially a workplace/company pension scheme. Generally set up by the company directors for themselves and other key or senior members of staff.

Contributions to a SSAS can be made by the individual and/or the company with both benefitting from tax relief.

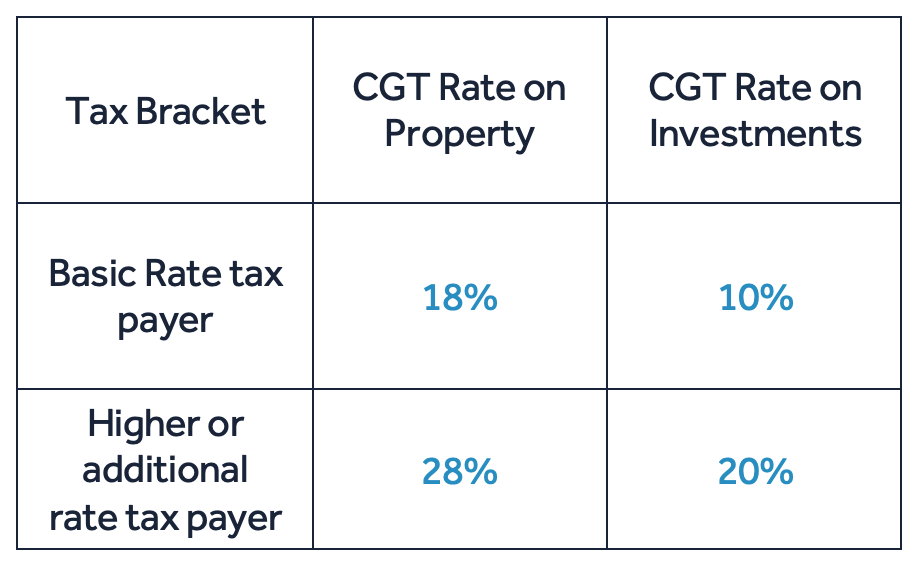

If your investments or investment property have increased in value, you might have to pay tax on the profit when you dispose of the investment. This is called Capital Gains Tax.

How much CGT you pay depends on whether you have made a profit, your current tax band and your CGT allowance. The Capital Gains Tax allowance for the tax year 2023-2024 is £6,000. This is set to move to £3,000 for the tax year 2024-2025.

If you make a loss when you sell, you might be able to offset this from other gains so your total gain is lower. You do not have to pay tax on investments held in an ISA or JISA.

We hold relationships with most of the major SIPP providers and can act as Investment Managers for you

Absolutely. It is a flexible ISA meaning that if you withdraw funds during the year, you are able to add them back in before year end

Income and disposals are tax free

A JISA account will turn into an adult ISA once the beneficial owner turns 18

The securities we invest in are liquid and funds can be withdrawn from the portfolio at any time if needed. The portfolio is marked with “IHT” for ease when accountants/solicitors view the estate to calculate taxes payable

We are able to access new issues from the top providers and buy or sell shares for you once they are listed

We have made it as simple as possible for you to open an account with us. If you need any assistance, you can contact us via our online messaging portal, however, if you would prefer to have a conversation over the phone, a member of our team would be delighted to help.