Well, what a year 2020 was! So much has already been written, but much more is still to be written about its consequences. Most obviously it represented a life-or-death challenge, particularly to the older and more vulnerable members of our society. However, it also had highly impactful economic and financial consequences. It has been a challenge for everyone, but its repercussions vary considerably. The pandemic has been a storm that we are all in but in different boats. This point is valid for investors as well as broader society. In this post, we look at 2020 equity market performance more closely to understand how best to prepare for the year ahead, and beyond.

In particular, 2020 was an exciting and challenging year for Dowgate’s most favoured asset class, UK smaller companies. Their general performance has been highlighted by Paul Marsh and Scott Evans of the London Business School, in their year-end analysis of the Numis Smaller Companies Index (NSCI).

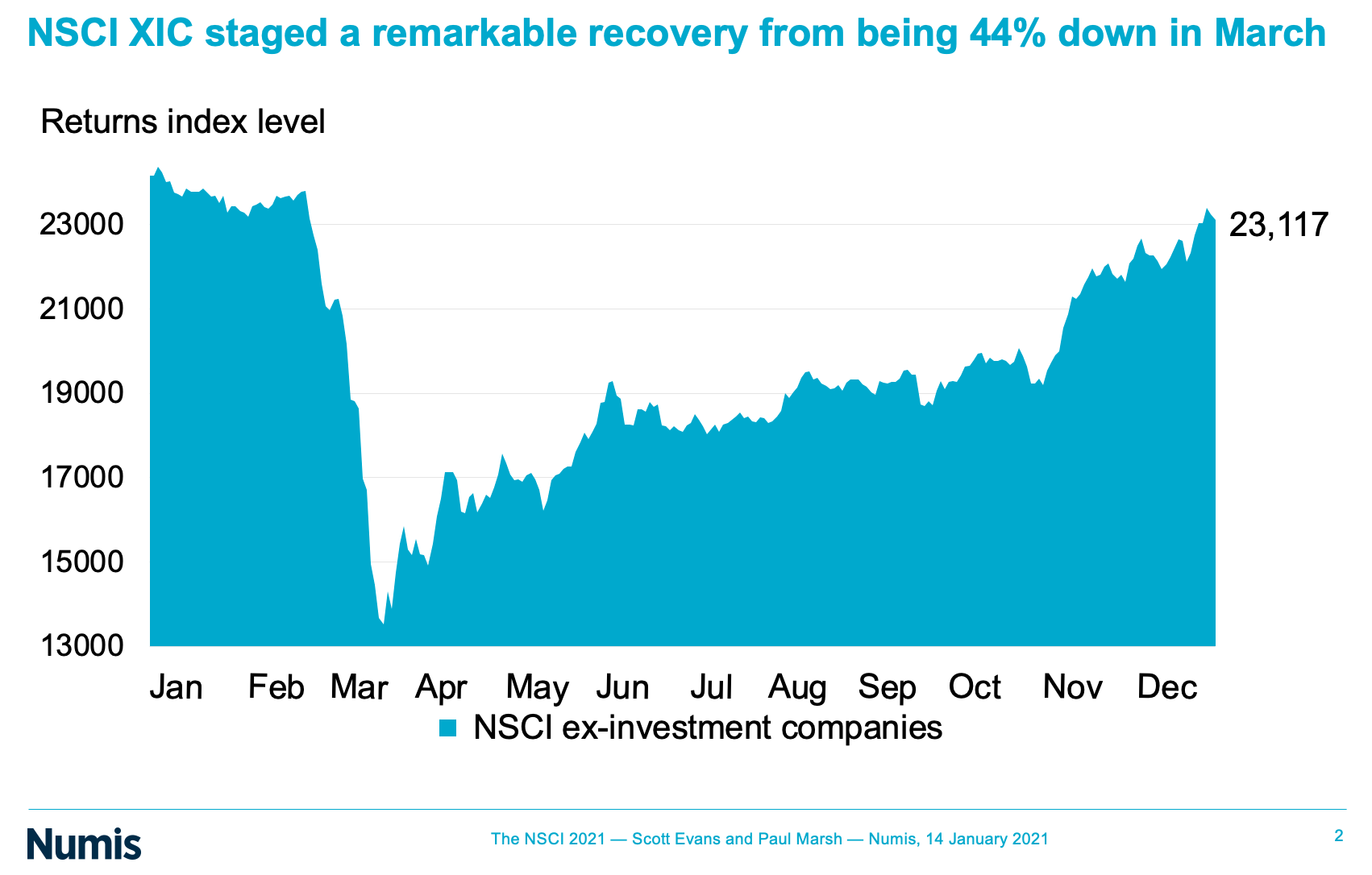

Having suffered a remarkable 44% pullback from mid-March, UK smaller companies ended the year just down 4%, ahead of the broader FT All Share measure.

However, we believe that the key to capturing the excess returns available to equity investors is patience. Taking a longer-term view, particularly with less liquid smaller cap stocks, irons out the volatility of returns and allows for the beneficial effect of compounding to accrue. To be a long-term investor it is essential to have conviction about the reasons we invest, thus making the emotional challenge of holding onto a position, that might go wrong in the short term, less stressful (albeit never easy).

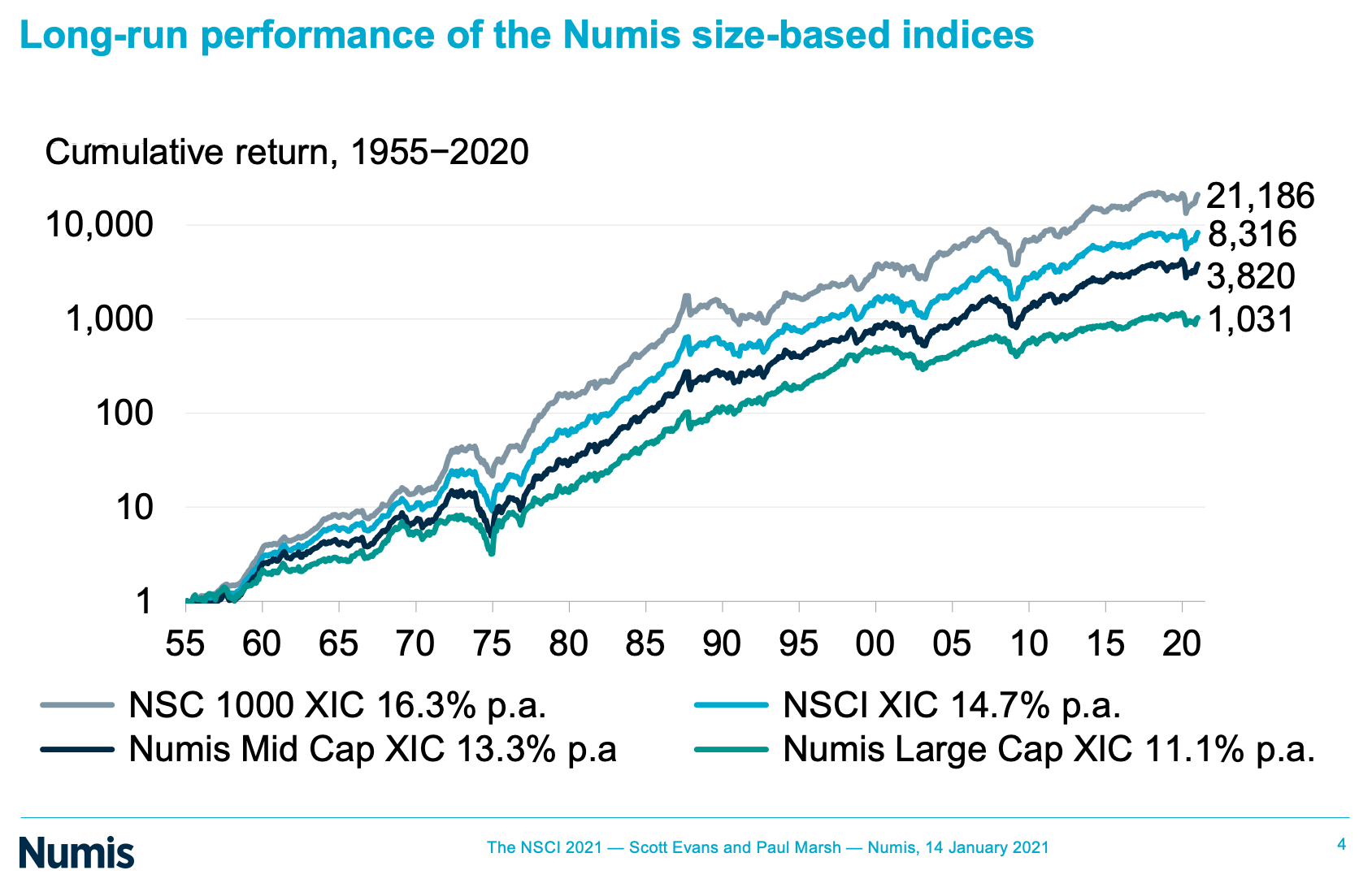

This critical factor to equity investing and the ability to assume (ride out) risk is illustrated by the time series of the leading Numis UK equity Indices over the long term, segmented by size.

This chart shows how £1 invested in 1955 into the bottom 2% by size (NSC 1000 XIC) of the UK equity market would be worth today over £21 000. This return compares to £8 000 for the bottom 10% (NSCI XIC), under £4 000 for the cohort between the bottom 5% and bottom 20% by size (Numis Mid Cap XIC) of the market and a mere £1 000 if invested in the top 10% by market value (Numis Large Cap XIC). A clear demonstration of what is known as the Smaller Company Effect, a key component of Dowgate’s investment strategy.

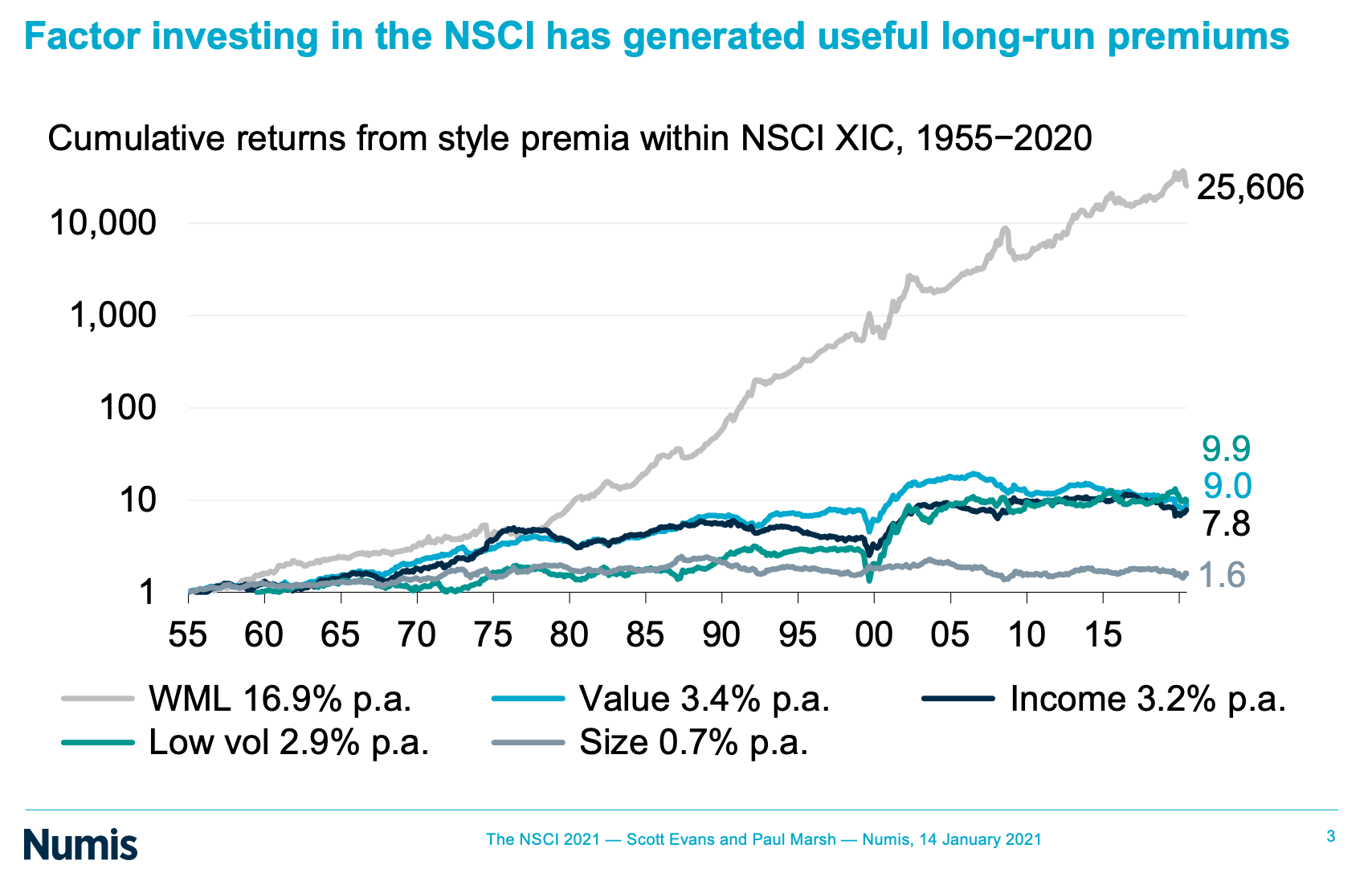

Helpfully the LBS team also segmented the historical data by broad (and theoretically defined) investment factor.

Here they compare five theoretical investment styles within the Numis Smaller Companies Index over the same period: Momentum (Winners Minus Losers); Value; Income; Low Volatility; and Size. Momentum, buying shares in the previous year’s winners and selling the losers, is the best performing long term strategy. Momentum decisively beats other traditional styles such as income and value. While it is dangerous to extrapolate too much from these theoretical exercises, it is illustrative. It demonstrates that while trying to capture the Smaller Company Effect, it pays to run winning stocks and cut losers (the key is knowing when to add to an undervalued winner and when to sell a confirmed loser). As you can see these lessons, are not exactly consistent. The reality is that stock selection and portfolio construction are a dynamic balancing act within these critical constraints.

So how was 2020 in this longer-term context? It was not exactly typical. The key message is that the UK equity market performed poorly by international comparisons, regardless of size. However, smaller companies outperformed larger ones. There was no significant return to factor type (or style) of investment over the year, indeed for the first time, all the factor types underperformed, with momentum running strongly in Q2 and Q3 and value recovering strongly in Q4. Digging deeper the UK equity market saw an increase in IPO activity (from very little to a bit more), a significant increase in equity financing activity (but still only a fraction of the amount in 2008-9), and saw a decline in the number of company failures. The overall hero performer in the UK equity market in 2020 was the AIM market (up 20% over the year). The most significant equity market negative in 2020, was dividend income, with NSCI dividends declining by a third, year on year (the most significant decline in 65 years).

There is quite a bit to unpack here, but in short, as we enter 2021, the UK equity market is looking attractively priced in the global context. A lot is being written about the US stock market’s unprecedented high level and its bubble-like characteristics (SPAC mania, Tesla, IPO pops and Robinhood day traders). However, the UK has not been part of this narrative. Since 2016 the £ and the UK equity market have primarily been risky outliers by global asset allocators due to a no-deal Brexit threat. Add to this the impact of a below-par initial response to COVID, the UK market may have followed in the path of Wall Street, but it has remained its poor relation. Warren Buffet’s favoured yardstick for measuring a country’s equity market value is the ratio of its equity market cap to GDP over time. While the US is at an all-time on this measure, the UK is only at 50% of its high, and remains 30% below the level seen in 2007. UK equities offer an attractive margin of safety relative to the US.

Indeed, higher US valuations have drawn out much higher IPO activity levels, creating a cycle of hype and upward re-rating as market confidence has been boosted by some extraordinary first day IPO returns. While there are signs that this cycle might have started in the UK, we are about 12 months behind. There is a strong list of UK IPO contenders set to follow in the path forged by The Hut Group, with Moon Pig and Doc Martens already declared and names like Deliveroo, Tranferwise and Trust Pilot lining up. As we get into 2021 with its global lead on vaccinations, the UK market and its new slate of attractive IPO candidates could be a catalyst to regenerate the UK equity market.

However, we should not get too far over our skis. This bullish investment trend is also likely to coincide with some other less positive trends such as increased company failures, emergency balance sheet repairs, further QE, and other monetary and fiscal stimuli, plus the likelihood of higher taxes and rising unemployment. All these things will be prevalent. The real test of solvency will come as COVID-19 support measures are phased out. As an economy, we will be over-invested in certain asset types. Shops, cinemas, and offices look like low return assets for a while. And under-invested in others, distribution warehousing, AI chips and high-quality care homes for the elderly. Cross Rail might not see quite such high initial passenger numbers, Heathrow won’t need that new runway. The economy needs a period of restructuring in which many companies and livelihoods will be lost, while others will bloom. It’s what Joseph Schumpeter called capitalism’s creative destruction.

The macroeconomic environment will remain complex and unknowable. Will interest rates stay low for a while? (probably); are we in an inflationary or deflationary cycle? (hard to know but probably inflationary, eventually); will the 40-year bond bull run end suddenly or slowly? (hard to know, but it is not going to run on for another 40 years); will we see the return of stubbornly high long-term unemployment? (probably not, but we might see things like Universal Basic Income); will we see greater investment levels boost labour productivity for the first time in over a decade? (maybe, eventually). While we might see the best short-term performance from low-value companies that just make it through this uncertain period, the best long-term risk adjusted returns will still come from high-quality businesses. High-quality businesses can benefit from, or adapt quickly to, a changing environment and continue compounding growth. The most obvious place to look for these opportunities is those sectors that are likely to get a short term re-opening boost. Rather than buying an indebted capital-intensive airline, choose a capital-light online travel agency with a long-term future of market share growth ahead of it.

We are all hoping 2021 will mark a return to a better normal. This is a sensible central case, but with virus mutation and other forms of uncertainty still apparent, we cannot be sure of the timing or trajectory. In equity markets, the margin of safety, resilience, and the ability to grow will remain critical factors to determine in which boats we chose to travel. However, UK smaller companies remain an excellent place to be selectively positioned.

Written by Jeremy McKeown