Market Mind Games – Most economic indicators point towards at least deceleration or stagnation, but not necessarily a recession. Elevated prices have led to demand destruction across a broad swathe of non-energy commodities. Investor sentiment is almost universally negative for risk assets, so bear market rallies can take hold quickly when incremental news is anything other than bad. On certain days financial markets perceive that inflation’s trajectory is flattening. Reducing expectations of Fed tightening give oversold risk assets a chance to recover, or at least stabilise. Investor interpretation of such days is either the start of recovery or aberrations in the endless longer-term downtrend. Investor mind games thus continue.

Money Supply Growth Halted – The world is being drained of liquidity. As liquidity declines, economic activity decelerates, defensive assets outperform, and cash outperforms risk assets. Specifically, the world is running short of US dollars. There has been much media coverage of the collapse of the GBP. But the primary global currency story has been the flight to the USD. The US is exporting inflation via its strengthening currency. With USD rates moving up rapidly, other currencies are being smoked. Most notably, the Yen, where the BoJ continues to fight the last war. Overall the world’s broad money supply growth has reached zero, having grown at over 20% over the period 2020/21. This is typically at least disinflationary if not deflationary.

Euro Crisis II – The ECB is showing signs of strain. A decade after the last Eurozone crisis, we might be about to get season two. This time Euro defender-in-chief Draghi has switched sides. His replacement Christine Lagard said last year that the ECB is not here to close spreads. But now, pulling a complete 180, she promises to deliver a new ECB “antifragmentation tool” by the next meeting. This new unexplained invention reminds me of AA Milne’s Train. Let it rain, — who cares? I’ve a train — upstairs, With a brake that I make from a string sorta thing — Which works — in jerks, ‘Cause it drops in the spring and it stops with the string, And that’s what I make when the day’s all wet, It’s a good sort of brake, but it hasn’t worked yet. But let’s see if she has a get out of jail free card.

Seeking Antifragile – While we have already had a valuation recession for equities, we have yet to see an impact on corporate earnings or earnings expectations. Company results and forward guidance are likely to justify many recently decimated valuations. The market might chop sideways for 3 to 6 months as investors digest lower numbers and reduced expectations. But at the individual stock level, the market liquidation will have produced anomalous moves. The focus should remain on high-quality business models and strong balance sheets that can emerge stronger from a recession. Resilience is good, antifragility is better.

The Cost of Staying Warm – Energy supply, particularly in Europe, remains stubbornly unresponsive to higher prices. Russia’s move to close Nordstream 1 for maintenance, a blatant attempt to prevent the seasonal rebuild of European gas inventories, is a reminder that geo-politics has added to our existing energy transition problem. But as we have been worrying about supply chain issues and shortages, we have unconsciously been filling our tanks and stocking our freezers and cupboards. Retailers and distributors have been doing the same. Amazon has over-invested in warehouse capacity, and Walmart and Target have recently admitted to being overstocked with (largely the wrong) products. US inventories have grown at the fastest rate in the past twenty years over the last quarter. We might be unable to afford to have the central heating on high this winter, but at least we should be able to buy jumpers and blankets at reasonable prices.

Pick a Letter – As investor fear shifts from inflation to a recession, the critical question becomes how deep and for how long? In the second half of 2020, commentators hailed us with an alphabet soup of recovery profiles to choose from. Were we entering a V, U, W or L-shaped recovery? Stuttering re-opening in 2021 with supply constraints has meant that an elongated W might be the best fit. The slowdown we are heading towards could yet be short-lived and even mild.

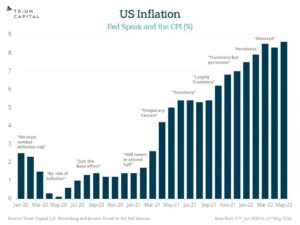

Meanwhile at the Federal Reserve – Longer-dated US index-linked bonds (TIPS) indicate that inflation could yet prove transitory. Jerome Powell stated the obvious this week when he said: I think we now understand better how little we understand about inflation. The chart below (courtesy of Trium Capital) puts this significant mea culpa from the world’s chief inflation officer into its proper context.

Written by Jeremy McKeown